In many industries, offering a 401(k) plan is a competitive necessity. If you don’t offer one and a competitor does, it could mean the difference in a job candidate’s decision to accept their offer over yours. It could even send employees heading for the door.

Assuming you do offer a 401(k), the challenge then becomes plan maintenance and compliance. Just as you presumably visit your doctor annually for a checkup, you should review the administrative processes and fiduciary procedures associated with your plan at least once a year. Let’s look at some important areas of consideration as advised by top business consultant:

Investments.Study your plan’s investment choices to determine whether the selections available to participants are appropriate. Does the lineup offer options along the risk-and-return spectrum for all ages of participants? Are any pre-mixed funds, which are based on age or expected retirement date, appropriate for your employee population?

If the plan includes a default investment for participants who have failed to direct investment contributions, check the option to ensure that it continues to be appropriate. If your company plan doesn’t have a written investment policy in place or doesn’t use an independent outside consultant to assist in selecting and monitoring investments, consider incorporating these into your investment procedures.

Fees.401(k) plan fees often come under criticism in the media and can aggravate employees who follow their accounts closely. Calculate the amount of current participant fees associated with your plan’s investments and benchmark them against industry standards.

Investment managers.Have you documented in writing the processes your plan has in place for the selection and monitoring of investment managers? If not, doing so in consultation with an attorney is highly advisable. If you have, reread the documents to ensure they’re still accurate and comprehensive.

Administrator.Solicit and monitor participant feedback on the administrator so that you know about grumblings before they grow into heated complaints. Further, put criteria in place to assess the plan administrator’s performance on an ongoing basis and to benchmark performance against industry standards.

Compliance.Are your plan’s administrative procedures in compliance with current regulations? If you intend your plan to be a participant-directed individual account plan, are all the provisions of ERISA Section 404(c) being followed? Have there been any major changes to 401(k) regulations over the last year? These are just a few critical questions to ask and answer.

A 401(k) is usually among the most valued benefits a business can offer its employees, but you’ve got to keep a close and constant eye on its details. We’d be happy to help you assess the costs and other financial details of your company’s plan.

Perhaps you’re an investor in mutual funds or you’re interested in putting some money into them, as a part of your tax strategy. You’re not alone. The Investment Company Institute estimates that 56.2 million households owned mutual funds in mid-2017. But despite their popularity, the tax rules involved in selling mutual fund shares can be complex.

Tax basics

If you sell appreciated mutual fund shares that you’ve owned for more than one year, the resulting profit will be a long-term capital gain. As such, themaximumfederal income tax rate will be 20%, and you may also owe the 3.8% net investment income tax.

When a mutual fund investor sells shares, gain or loss is measured by the difference between the amount realized from the sale and the investor’s basis in the shares. One difficulty is that certain mutual fund transactions are treated as sales even though they might not be thought of as such. Another problem may arise in determining your basis for shares sold.

What’s considered a sale

It’s obvious that a sale occurs when an investor redeems all shares in a mutual fund and receives the proceeds. Similarly, a sale occurs if an investor directs the fund to redeem the number of shares necessary for a specific dollar payout.

It’s less obvious that a sale occurs if you’re swapping funds within a fund family. For example, you surrender shares of an Income Fund for an equal value of shares of the same company’s Growth Fund. No money changes hands but this is considered a sale of the Income Fund shares.

Another example: Many mutual funds provide check-writing privileges to their investors. However, each time you write a check on your fund account, you’re making a sale of shares.

Determining the basis of shares

If an investor sells all shares in a mutual fund in a single transaction, determining basis is relatively easy. Simply add the basis of all the shares (the amount of actual cash investments) including commissions or sales charges. Then add distributions by the fund that were reinvested to acquire additional shares and subtract any distributions that represent a return of capital.

The calculation is more complex if you dispose of only part of your interest in the fund and the shares were acquired at different times for different prices. You can use one of several methods to identify the shares sold and determine your basis.

First-in first-out.The basis of the earliest acquired shares is used as the basis for the shares sold. If the share price has been increasing over your ownership period, the older shares are likely to have a lower basis and result in more gain.

Specific identification.At the time of sale, you specify the shares to sell. For example, “sell 100 of the 200 shares I purchased on June 1, 2015.” You must receive written confirmation of your request from the fund. This method may be used to lower the resulting tax bill by directing the sale of the shares with the highest basis.

Average basis.The IRS permits you to use the average basis for shares that were acquired at various times and that were left on deposit with the fund or a custodian agent.

As you can see, mutual fund investing can result in complex tax situations. Contact us if you have questions. We can explain in greater detail how the rules apply to you.

The Setting Every Community Up for Retirement Enhancement (SECURE) Act is the first significant retirement-related legislation in more than a dozen years. It brings many changes that affect employers of all sizes, including some that could be particularly beneficial for smaller employers that sponsor retirement plans. Some of the changes, however, may increase the burden on employers. Here are some of the most important developments for employers, many of which took effect for plan years beginning after December 31, 2019. Please read and see how it can help you design tax strategies for this year

Greater access to multiple employer plans

Multiple employer plans (MEPs) allow small and midsize unrelated businesses to team up to provide their employees a defined contribution plan, such as a 401(k) or SIMPLE IRA plan. By pooling plan participants and assets in one large plan, rather than several separate plans, it’s possible for small businesses to give their workers access to the same low-cost plans offered by large employers. Employers enjoy reduced fiduciary duties and administrative burdens by using outside administrators to manage the plan.

Currently, MEPs generally are limited to participating employers that share some commonality – for example, being in the same industry or geographic location or using the same professional employer organization. The SECURE Act creates a new type of “open MEP” that covers employees of employers with no relationship other than their joint participation in the MEP. These pooled employer plans (PEPs) will be administered by a pooled plan provider (PPP), such as a financial services company. The PPP also will be the named fiduciary of the plan, but each employer is responsible for choosing and monitoring the PPP.

PEPs will be permitted for plan years starting in 2021 or later. The U.S. Department of Labor and the IRS are expected to provide guidance before then, as PEPs generally are subject to the same Employee Retirement Income Security Act (ERISA) and Internal Revenue Code rules as single-employer plans.

In addition, the SECURE Act eliminates the so-called “one bad apple” rule that deterred some employers from taking advantage of MEPs. Under the rule, a regulatory violation by one employer participant (such as failing to make contributions to the plan on schedule) could jeopardize the MEP’s tax-qualified status. The SECURE Act lays out certain requirements that a PEP can satisfy to protect its status in such a situation.

The SECURE Act also provides an alternative to MEPs for small employers seeking the economies of scale they provide regarding administration. It allows a group of plans with a common plan administrator to file a consolidated Form 5500 annual report, with a single audit report, if certain conditions are met.

Looser notice and amendment rules on safe harbor plans

As of January 1, 2020, plan sponsors no longer are required to give notice to plan participants before the beginning of the plan year when the sponsor is making qualified nonelective contributions – that is, contributions an employer makes regardless of whether an employee contributes – of at least 3% to all eligible participants. The requirement to provide advance notice when making safe harbor matching contributions continues.

Plan sponsors also can amend 401(k) plans that don’t use a matching contribution safe harbor to include a 3% nonelective contribution safe harbor any time before the 30th day before the end of the plan year. The amendment can be made later than that only if it provides for a qualified nonelective contribution of at least 4% of compensation, rather than 3%, and the amendment is done no later than the close of the following plan year.

Annuity options

Annuities can help reduce the risk that retirees will run out of money before the last years of their lives, when health care expenses can run high. But many employers have been reluctant to offer annuities for fear of facing lawsuits alleging breach of fiduciary duty if the annuity providers they selected run into financial problems down the road. The SECURE Act preempts this hurdle by immunizing employers from liability if they choose a provider that meets certain requirements, starting December 20, 2019.

The SECURE Act, however, also requires employers to include a lifetime income disclosure on a plan participant’s benefit statements at least annually. The disclosure will show the estimated monthly payments the participant would receive if the total account balance were used to purchase an annuity for the participant and his or her surviving spouse. Before employers can implement this requirement, the U.S. Department of Labor must issue applicable guidance.

Participation by part-time employees

Employers generally have been allowed to exclude employees who work fewer than 1,000 hours per year from defined contribution plans, including 401(k) plans. Starting in 2021, the SECURE Act generally expands the rule by requiring employers to allow not just those who work at least 1,000 hours in one year (about 20 hours per week) to participate, but also those who work at least 500 hours in three consecutive years and are at least age 21 at the end of the three-year period.

Employer contributions aren’t a requirement of the new participation rules for part-time employees. And employers can exclude the latter category of part-time employees from testing under the nondiscrimination and coverage rules, as well as from the application of the top-heavy rules.

Expanded tax credits

The SECURE Act establishes a new tax credit of up to $500 per year to offset start-up costs for new 401(k) and SIMPLE IRA plans with an eligible automatic contribution arrangement (EACA), beginning in 2020. This credit is on top of the plan start-up credit already available and is available for three years. It’s also available to employers that convert an existing plan to one with an EACA.

The new law also boosts the amount of the credit available for small employer pension plan start-up costs. (A “small employer” is one with no more than 100 employees.) The new law changes the calculation of the flat dollar amount limit on the credit to the greater of 1) $500 or 2) the lesser of:

$250 multiplied by the number of non-highly compensated employees who are eligible to participate in the plan, or

$5,000.

Like the automatic enrollment tax credit, it’s available beginning in 2020 and applies for up to three years.

Higher automatic enrollment safe harbor cap

Even before the SECURE Act, employers could automatically enroll employees in a 401(k) plan under a safe harbor with a qualified automatic contribution arrangement (QACA). However, elective deferrals for QACAs have been limited to 10% of compensation.

The SECURE Act increases the maximum amount of an employee’s compensation that can be automatically deferred after the employee’s first plan year, from 10% to 15%. (The cap for the first year in the plan is 10%.) The increase is effective for plan years beginning after December 31, 2019.

Adoption deadlines

Previously, many types of retirement plans were required to be set up during the tax year for which they were to take effect. The SECURE Act extends the adoption deadline for a tax year to the due date of the employer’s tax return (including extensions), providing more flexibility to make contributions and reduce tax liabilities.

Costlier penalties

The SECURE Act increases the penalties for failing to file retirement plan tax returns, as follows:

The penalty for failing to file a Form 5500 is $250 per day, not to exceed $150,000 (up from $25 per day, with a maximum of $15,000).

The penalty for failing to file a registration statement (IRS Form 8955-SSA) is $10 per participant per day, not to exceed $50,000 (up from $1 per participant per day, with a maximum of $5,000).

The penalty for failure to provide a notification of change of certain information (for example, the plan name, sponsor or administrator) is $10 per day, not to exceed $10,000 (up from $1 per day, with a maximum of $1,000).

The penalty for failing to provide a required withholding notice is $100 for each failure, not to exceed $50,000 for all failures during any calendar year (up from $10 for each failure, with a maximum of $5,000).

The penalty hikes apply for filings, registrations and notifications required after December 31, 2019.

Promising, but complicated

These and other changes in the SECURE Act are intended to make it easier and less expensive for employers to offer retirement plans to their employees. (The law also contains a number of significant changes for individuals.) The applicable laws and regulations can prove tricky to navigate. Please contact us with any questions regarding the SECURE Act.

If you’re gearing up for your Tax return preparation to file your 2019 tax return, and your tax bill is higher than you’d like, there may still be an opportunity to lower it. If you qualify, you can make a deductible contribution to a traditional IRA right up until the Wednesday, April 15, 2020, filing date and benefit from the resulting tax savings on your 2019 return.

Do you qualify?

You can make a deductible contribution to a traditional IRA if:

You (and your spouse) aren’t an active participant in an employer-sponsored retirement plan, or

You (or your spouse) are an active participant in an employer plan, and your modified adjusted gross income (AGI) doesn’t exceed certain levels that vary from year-to-year by filing status.

For 2019, if you’re a joint tax return filer covered by an employer plan, your deductible IRA contribution phases out over $103,000 to $123,000 of modified AGI. If you’re single or a head of household, the phaseout range is $64,000 to $74,000 for 2019. For married filing separately, the phaseout range is $0 to $10,000. For 2019, if you’re not an active participant in an employer-sponsored retirement plan, but your spouse is, your deductible IRA contribution phases out with modified AGI of between $193,000 and $203,000.

Deductible IRA contributions reduce your current tax bill, and earnings within the IRA are tax deferred. However, every dollar you take out is taxed in full (and subject to a 10% penalty before age 59 1/2, unless one of several exceptions apply).

IRAs often are referred to as “traditional IRAs” to distinguish them from Roth IRAs. You also have until April 15 to make a Roth IRA contribution. But while contributions to a traditional IRA are deductible, contributions to a Roth IRA aren’t. However, withdrawals from a Roth IRA are tax-free as long as the account has been open at least five years and you’re age 59 1/2 or older.

Here are a couple other IRA strategies that might help you save tax.

1. Turn a nondeductible Roth IRA contribution into a deductible IRA contribution.Did you make a Roth IRA contribution in 2019? That may help you years down the road when you take tax-free payouts from the account. However, the contribution isn’t deductible. If you realize you need the deduction that a traditional IRA contribution provides, you can change your mind and turn that Roth IRA contribution into a traditional IRA contribution via the “recharacterization” mechanism. The traditional IRA deduction is then yours if you meet the requirements described above.

2. Make a deductible IRA contribution, even if you don’t work.In general, you can’t make a deductible traditional IRA contribution unless you have wages or other earned income. However, an exception applies if your spouse is the breadwinner and you manage the home front. In this case, you may be able to take advantage of a spousal IRA.

How much can you contribute?

For 2019 if you’re qualified, you can make a deductible traditional IRA contribution of up to $6,000 ($7,000 if you’re 50 or over).

In addition, small business owners can set up and contribute to a Simplified Employee Pension (SEP) plan up until the due date for their returns, including extensions. For 2019, the maximum contribution you can make to a SEP account is $56,000.

If you’d like more information about whether you can contribute to an IRA or SEP, contact us or ask about it when we’re preparing your return. We’d be happy to explain the rules and help you save the maximum tax-advantaged amount for retirement.

Right now, you may be more concerned about your 2019 tax bill than you are about your 2020 tax situation. That’s understandable because your 2019 individual tax return is due to be filed in less than three months.

However, as Business Consultant we suggest that it’s a good idea to familiarize yourself with tax-related amounts that may have changed for 2020. For example, the amount of money you can put into a 401(k) plan has increased and you may want to start making contributions as early in the year as possible because retirement plan contributions will lower your taxable income.

Note: Not all tax figures are adjusted for inflation and even if they are, they may be unchanged or change only slightly each year due to low inflation. In addition, some tax amounts can only change with new tax legislation.

So below are some Q&As about tax-related figures for this year.

How much can I contribute to an IRA for 2020?

If you’re eligible, you can contribute $6,000 a year into a traditional or Roth IRA, up to 100% of your earned income. If you’re age 50 or older, you can make another $1,000 “catch up” contribution. (These amounts are the same as they were for 2019.)

I have a 401(k) plan through my job. How much can I contribute to it?

For 2020, you can contribute up to $19,500 (up from $19,000) to a 401(k) or 403(b) plan. You can make an additional $6,500 catch-up contribution if you’re age 50 or older.

I sometimes hire a babysitter and a cleaning person. Do I have to withhold and pay FICA tax on the amounts I pay them?

In 2020, the threshold when a domestic employer must withhold and pay FICA for babysitters, house cleaners, etc. is $2,200 (up from $2,100 in 2019).

How much do I have to earn in 2020 before I can stop paying Social Security on my salary?

The Social Security tax wage base is $137,700 for this year (up from $132,900 last year). That means that you don’t owe Social Security tax on amounts earned above that. (You must pay Medicare tax on all amounts that you earn.)

I didn’t qualify to itemize deductions on my last tax return. Will I qualify for 2020?

The Tax Cuts and Jobs Act eliminated the tax benefit of itemizing deductions for many people by increasing the standard deduction and reducing or eliminating various deductions. For 2020, the standard deduction amount is $24,800 for married couples filing jointly (up from $24,400). For single filers, the amount is $12,400 (up from $12,200) and for heads of households, it’s $18,650 (up from $18,350). So if the amount of your itemized deductions (such as charitable gifts and mortgage interest) are less than the applicable standard deduction amount, you won’t itemize for 2020.

How much can I give to one person without triggering a gift tax return in 2020?

The annual gift exclusion for 2020 is $15,000 and is unchanged from last year. This amount is only adjusted in $1,000 increments, so it typically only increases every few years.

Your tax picture

These are only some of the tax figures that may apply to you. For more information about your tax picture, or if you have questions, don’t hesitate to contact us.

If you save for retirement with an IRA or other plan, you’ll be interested to know that Congress recently passed a law that makes significant modifications to these accounts. The SECURE Act, which was signed into law on December 20, 2019, made these four changes, lets read about these changes and see how they can benefit in Tax return preparation.

Change #1: The maximum age for making traditional IRA contributions is repealed.Before 2020, traditional IRA contributions weren’t allowed once you reached age 70½. Starting in 2020, an individual of any age can make contributions to a traditional IRA, as long he or she has compensation, which generally means earned income from wages or self-employment.

Change #2: The required minimum distribution (RMD) age was raised from 70½ to 72.Before 2020, retirement plan participants and IRA owners were generally required to begin taking RMDs from their plans by April 1 of the year following the year they reached age 70½. The age 70½ requirement was first applied in the early 1960s and, until recently, hadn’t been adjusted to account for increased life expectancies.

For distributions required to be made after December 31, 2019, for individuals who attain age 70½ after that date, the age at which individuals must begin taking distributions from their retirement plans or IRAs is increased from 70½ to 72.

Change #3: “Stretch IRAs” were partially eliminated.If a plan participant or IRA owner died before 2020, their beneficiaries (spouses and non-spouses) were generally allowed to stretch out the tax-deferral advantages of the plan or IRA by taking distributions over the beneficiary’s life or life expectancy. This is sometimes called a “stretch IRA.”

However, for deaths of plan participants or IRA owners beginning in 2020 (later for some participants in collectively bargained plans and governmental plans), distributions to most non-spouse beneficiaries are generally required to be distributed within 10 years following a plan participant’s or IRA owner’s death. That means the “stretch” strategy is no longer allowed for those beneficiaries.

There are some exceptions to the 10-year rule. For example, it’s still allowed for: the surviving spouse of a plan participant or IRA owner; a child of a plan participant or IRA owner who hasn’t reached the age of majority; a chronically ill individual; and any other individual who isn’t more than 10 years younger than a plan participant or IRA owner. Those beneficiaries who qualify under this exception may generally still take their distributions over their life expectancies.

Change #4: Penalty-free withdrawals are now allowed for birth or adoption expenses.A distribution from a retirement plan must generally be included in income. And, unless an exception applies, a distribution before the age of 59½ is subject to a 10% early withdrawal penalty on the amount includible in income.

Starting in 2020, plan distributions (up to $5,000) that are used to pay for expenses related to the birth or adoption of a child are penalty-free. The $5,000 amount applies on an individual basis. Therefore, each spouse in a married couple may receive a penalty-free distribution up to $5,000 for a qualified birth or adoption.

Questions?

These are only some of the changes included in the new law. If you have questions about your situation, don’t hesitate to contact us.

A good news for all of those who are planning their Tax Return preparation, as part of a year-end budget bill, Congress just passed a package of tax provisions that will provide savings for some taxpayers. The White House has announced that President Trump will sign the Further Consolidated Appropriations Act of 2020 into law. It also includes a retirement-related law titled the Setting Every Community Up for Retirement Enhancement (SECURE) Act.

Here’s a rundown of some provisions in the two laws.

The age limit for making IRA contributions and taking withdrawals is going up.Currently, an individual can’t make regular contributions to a traditional IRA in the year he or she reaches age 70½ and older. (However, contributions to a Roth IRA and rollover contributions to a Roth or traditional IRA can be made regardless of age.)

Under the new rules, the age limit for IRA contributions is raised from age 70½ to 72.

The IRA contribution limit for 2020 is $6,000, or $7,000 if you’re age 50 or older (the same as 2019 limit).

In addition to the contribution age going up, the age to take required minimum distributions (RMDs) is going up from 70½ to 72.

It will be easier for some taxpayers to get a medical expense deduction.For 2019, under the Tax Cuts and Jobs Act (TCJA), you could deduct only the part of your medical and dental expenses that is more than 10% of your adjusted gross income (AGI). This floor makes it difficult to claim a write-off unless you have very high medical bills or a low income (or both). In tax years 2017 and 2018, this “floor” for claiming a deduction was 7.5%. Under the new law, the lower 7.5% floor returns through 2020.

If you’re paying college tuition, you may (once again) get a valuable tax break.Before the TCJA, the qualified tuition and related expenses deduction allowed taxpayers to claim a deduction for qualified education expenses without having to itemize their deductions. The TCJA eliminated the deduction for 2019 but now it returns through 2020. The deduction is capped at $4,000 for an individual whose AGI doesn’t exceed $65,000 or $2,000 for a taxpayer whose AGI doesn’t exceed $80,000. (There are other education tax breaks, which weren’t touched by the new law, that may be more valuable for you, depending on your situation.)

Some people will be able to save more for retirement.The retirement bill includes an expansion of the automatic contribution to savings plans to 15% of employee pay and allows some part-time employees to participate in 401(k) plans.

Also included in the retirement package are provisions aimed at Gold Star families, eliminating an unintended tax on children and spouses of deceased military family members.

Stay tuned

These are only some of the provisions in the new laws. We’ll be writing more about them in the near future. In the meantime, contact us with any questions.

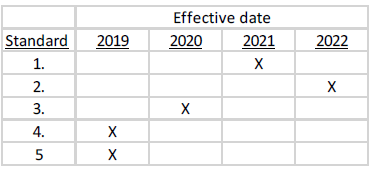

For 2019, there is a new accounting rule for revenue recognition that applies to non-public companies. In addition, there are other accounting rules for coming years. It is important to know these changes as they will change your accounting and financials and will help in Tax preparation services. Most banks, lenders, and investors want to see Generally Accepted Accounting Principles (GAAP) financial statements. Having GAAP financial statements allows a reader to use standard GAAP reporting to understand your financial statements, apply financial ratios and compare to industry ratios. Be prepared and contact us if we can assist.

Background

In May 2014, the Financial Accounting Standards Board (FASB) and International Accounting Standards Board (IASB) issued substantially converged final standards on revenue recognition. These final standards were the culmination of a joint project between the Boards that spanned many years. The FASB’s Accounting Standards Update (ASU) 2014-09, Revenue from Contracts with Customers (Topic 606), provides a robust framework for addressing revenue recognition issues, and upon its effective date, replaces almost all pre-existing revenue recognition guidance in current U.S. generally accepted accounting principles (GAAP). Implementation of the robust framework provided by ASU 2014-09 should result in improved comparability of revenue recognition practices across entities, industries, jurisdictions and capital markets. The effective dates for the new guidance are staggered. Public entities have already implemented the new guidance, and nonpublic entities are required to implement the new guidance in their first annual reporting period beginning after December 15, 2018.

Scope

All customer contracts fall within the scope of ASC 606 except those for which other guidance is provided in the ASC (e.g., leases, insurance contracts, financial instruments, guarantees, non-monetary exchanges).

Core principle and key steps

Revenue is now recognized in a five-step process:

Identify the contract with the customer

Identify the performance obligations in the contract

Determine the transaction price

Allocate the transaction price to the performance obligations

Recognize revenue when (or as) each performance obligation us satisfied.

LEASES

Starting in 2021, there is a new accounting rule for leases that applies to non-public companies. Early adoption is allowed and recommended. Although this new standard doesn’t need to be implemented for private companies until 2021, we are recommending applying it for 2020, so the company will have comparable financial statements for 2021. We feel this law is mean to get the lease liability on the balance sheet. For income taxes, a different method will probably apply.

Background

In February 2016, the FASB issued Accounting Standards Update No. 2016-02, Leases (Topic 842). The new standard requires that all leases should result in an asset and corresponding liability be recognized on the balance sheet. This asset reflects the right to use an asset that is owned by someone else. A corresponding liability reflecting future lease payments is also recognized on the balance sheet.

Scope

All leases with a lease term of over 12 months

Core principle and key steps

Capital leases are now called finance leases and the reporting of these types of leases did not significantly change.

Operating leases are now shown on the balance sheet as a liability and a right to use asset for the present value of the future lease payments.

OTHER NEW PRONOUNCEMENTS

Accounting Standards Update No. 2018-17- Private Company Council (PCC) recommended change to simplify the variable interest entity rules for non-public companies- real estate leased to a related party does not have to be combined now under certain circumstances. Early adoption is permitted. A variable interest entity is a related party entity that cannot stand on its own without a significant financial interest from the related entity.

Accounting Standards Update No. 2017-04-Simplifying the Test for Goodwill Impairment – Step 2 of the goodwill impairment test was eliminated in order to simplify the test for accounting. Early adoption is permitted. Since 2015, private companies have been allowed the option to amortize goodwill over 10 years, but, if the impairment test is still in place, rather than amortization, then step 2 of the impairment process has been eliminated. Step 2 included determining the implied fair value of goodwill and comparing it with the carrying amount of that goodwill.

Accounting Standards Update No. 2018-07-Non-employee stock-based compensation – Simplifies, updates and aligns non-employee stock-based compensation with employee accounting.

Accounting Standards Update No. 2016-15 Cash flow classification –. Aims to eliminate the diversity in practice related to the classification of certain cash receipts and payments.

Accounting Standards Update No. 2016-18 Restricted cash – Eliminates diversity in the classification of restricted cash on the balance sheet and classification and presentation of changes in restricted cash on the cash flows statement.

The table below shows the effective dates for these other new pronouncements:

Summary:

In summary, we are providing you with some information about some new accounting changes. Other changes may be required, so please contact us to discuss the application of these accounting changes and to review your financial statements if we are not already. This memo is meant to provide you with information on accounting changes, we are not providing accounting advice.

If you’re starting to fret about your 2019 tax bill, there’s good news – you may still have time to reduce your liability if you do your tax return preparation carefully. Three strategies are available that may help you cut your taxes before year-end, including:

1. Accelerate deductions/defer income.Certain tax deductions are claimed for the year of payment, such as the mortgage interest deduction. So, if you make your January 2020 payment this month, you can deduct the interest portion on your 2019 tax return (assuming you itemize).

Pushing income into the new year also will reduce your taxable income. If you’re expecting a bonus at work, for example, and you don’t want the income this year, ask if your employer can hold off on paying it until January. If you’re self-employed, you can delay your invoices until late in December to divert the revenue to 2020.

You shouldn’t pursue this approach if you expect to land in a higher tax bracket next year. Also, if you’re eligible for the qualified business income deduction for pass-through entities, you might reduce the amount of that deduction if you reduce your income.

2. Maximize your retirement contributions.What could be better than paying yourself instead of Uncle Sam? Federal tax law encourages individual taxpayers to make the maximum allowable contributions for the year to their retirement accounts, including traditional IRAs and SEP plans, 401(k)s and deferred annuities.

For 2019, you generally can contribute as much as $19,000 to 401(k)s and $6,000 for traditional IRAs. Self-employed individuals can contribute up to 25% of your net income (but no more than $56,000) to a SEP IRA.

3. Harvest your investment losses.Losing money on your investments has a bit of an upside – it gives you the opportunity to offset taxable gains. If you sell under-performing investments before the end of the year, you can offset gains realized this year on a dollar-for-dollar basis.

If you have more losses than gains, you generally can apply up to $3,000 of the excess to reduce your ordinary income. Any remaining losses are carried forward to future tax years.

We can help

The strategies described above are only a sampling of strategies that may be available. Contact us if you have questions about these or other methods for minimizing your tax liability for 2019.

The first tax-filing season under the Tax Cuts and Jobs Act (TCJA) was a time of uncertainty for many businesses as they struggled with the implications of the law’s sweeping changes for their bottom lines. With the next filing season on the horizon, you can incorporate the lessons learned into your Tax return preparation. Several areas in particular are ripe with opportunities to reduce your 2019 federal tax liability.

Entity choice

The creation of the qualified business income (QBI) deduction for pass-through entities, paired with the reduction of the corporate tax rate to a flat 21% rate from a top rate of 35%, make it worthwhile to re-evaluate whether your current entity type is the most tax-favorable.

Pass-through entities, including sole proprietorships, partnerships and S corporations, traditionally have been seen as a way to avoid the double taxation C corporations are subject to at the entity and dividend levels. Pass-through entities are taxed only once, at an individual tax rate, but that rate can be as high as 37%. If they qualify for the full 20% QBI deduction – not always a sure thing (see below) – their effective tax rate is about 30%.

The deduction for state and local taxes also plays a role in the entity choice. The TCJA limits the amount of the deduction for individual pass-through entity owners, but not for corporations.

Bear in mind, too, that the reduced corporate tax rate is permanent (or as permanent as any tax cut can be), while the QBI deduction is slated to end after 2025. Ultimately, your business’s individual circumstances will determine the optimal structure.

The QBI deduction

Pass-through entities can take several steps before December 31 to maximize their QBI deduction. The deduction is subject to phased-in limitations based on W-2 wages paid (including many employee benefits), the unadjusted basis of qualified property and taxable income. You could boost your deduction, therefore, by increasing wages (for example, by hiring new employees, giving raises or making independent contractors employees). To increase your adjusted basis, you can invest in qualified property by year end.

If the W-2 wages limitation doesn’t limit the QBI deduction, S corporation owners can increase their QBI deductions by reducing the amount of wages the business pays them. (This tactic won’t work for sole proprietorships or partnerships, because they don’t pay their owners salaries.) On the other hand, if the W-2 wages limitation limits the deduction, they might be able to take a greater deduction byincreasing their wages.

Tax credits

Some of the most popular tax credits for businesses survived the tax overhaul, including the Work Opportunity Tax Credit (WOTC), the Small Business Health Care tax credit, the New Markets Tax Credit (NMTC) and the research credit (also referred to as the “research and development,” “R&D” or “research and experimentation” credit). Smaller businesses may qualify for a credit for starting new retirement plans.

The WOTC, generally worth a maximum of $2,400 per employee (although for certain employees that can increase to $9,600), is currently scheduled to expire on December 31, so make those qualified hires before year end. The NMTC – 39% over seven years – also is set to expire at year end.

Capital asset investments

Purchasing equipment and other qualified capital assets has been a valuable tool for reducing taxable income for years, but the TCJA further greased the wheels by expanding bonus depreciation and Section 179 expensing (that is, deducting the entire cost in the current tax year).

For qualified property purchased after September 27, 2017, and before January 1, 2023, you can deduct the entire cost of new and used (subject to certain conditions) qualified property in the year the property is placed in service. Special rules apply to property with a longer production period.

Eligible property includes computer systems, computer software, vehicles, machinery, equipment and office furniture. Starting in 2023, the amount of the deduction will drop 20% each year going forward, disappearing altogether in 2027, absent congressional action.

Congress has thus far failed to take action to correct a drafting error in the TCJA that leaves qualified improvement property (generally interior improvements to nonresidential real property) ineligible for bonus deprecation.

Qualified improvement property is, however, eligible for Sec. 179 expensing. The TCJA makes this expensing available to several improvements to nonresidential real property, including roofs, HVAC, fire protection systems, alarm systems and security systems. It also increases the maximum deduction for qualifying property: For 2019, the limit is $1.02 million. (The maximum deduction is limited to the amount of income from business activity.) The expensing deduction begins phasing out on a dollar-for-dollar basis when qualifying property placed in service this year exceeds $2.55 million.

Deferring income / accelerating expenses

This technique has long been employed by businesses that don’t expect to be in a higher tax bracket the following year. If you use cash-basis accounting, for example, you might defer income into 2020 by sending your December invoices toward the end of the month. (Note that the TCJA now allows businesses with three-year average annual gross receipts of $25 million or less to use cash-basis accounting.) If your accounting is done on an accrual basis, you could delay delivery of goods and services until January.

Any business can accelerate deductible expenses into 2019 by putting them on a credit card in late December and paying it off in 2020 (subject to limitations). And cash-basis businesses can prepay bills due in January, as well as certain other expenses. Some caveats now apply to this approach. First, it could affect the amount of the QBI deduction for pass-through entities. It might make more sense to maximize the deduction while it’s still around – the deduction currently is scheduled to sunset after 2025 and, depending on the results of the 2020 elections, could be eliminated before then. Moreover, this tactic isn’t advisable if you’re likely to face higher tax rates in the future.

Act now

You still have time to make a significant dent in your business’s federal tax liability for 2019. We can help you chart the best course forward to minimize your tax bill and put you on solid ground for upcoming tax years.