As we’re all aware, 2020 has been an extraordinarily complex year — that complexity is reflected in taxpayers’ tax situations, whether they’re businesses or individuals. While there is plenty of time before this year’s tax returns need to be filed, the constantly changing economic situation, the presidential election, and the host of COVID-19 legislative provisions mean that some tax moves will only be effective if they’re made before the end of the year.

We’ve brought together some of our best year-end tax-planning coverage, ranging from reminders of classic strategies to deep dives into rules specific to COVID-19 tax relief. For each article, we’ve highlighted a strategy or two, but they all offer a host of potential tax savings — for those who act fast.

For businesses and individuals:

In early October, Top 10 Firm Grant Thornton put together a list, a mix of strategies for both companies and individual taxpayers, including:

Making sure to use the above-the-line charitable deduction

Accelerating AMT refunds

Taking advantage of new bonus depreciation rules from the CARES Act

New for the end of the year:

In an interview, Wolters Kluwer’s Mark Luscombe dives into some of the most important new year-end planning issues, including:

Employee tax credits and deferrals related to payroll taxes that expire at the end of 2020

Tax provisions that offer retroactive relief

The implementing expiration of the expanded ability to make penalty-free withdrawals from retirement plans

Expiring Relief:

With a number of COVID-19 related tax relief provisions, Laura Davison of Bloomberg News talks about how year-end planning has been turbocharged. Here are the provisions set to expire:

The removal of the cap on individuals’ business loss deductions

The one-time deduction for charitable gifts for taxpayers taking the standard deduction

Planning around the election:

Tax planners knew that the November election could have a major impact on year-end planning. Particularly, if a Biden win brought in a whole new approach to tax legislation. Accounting Today columnist Mark Luscombe, of Wolters Kluwer, offered strategies for both possible outcomes in Georgia, including:

With a Republic win, focusing more on tax-loss harvesting and less on Roth IRA conversions

With a Democratic win, preparing for the possibility of higher capital gains and income tax rates

Three-quarters of the way there:

In a column just before the election, Wolters Kluwer’s Mark Luscombe summarized the year-end planning developments thus far in the year including:

The restoration of NOL carrybacks for up to five years

A number of COVID related corrections and extensions to the Tax Cuts and Job Acts of 2017

COVID-19 sick leave and family leave, and employee retention provisions

Acceleration and declaration:

After a “year like no other” this early December list from AG FinTax’s Anil Grandhi included tips on lowering taxes by:

Accelerating business purchases

Adding children or spouses to the payroll

Deferring or accelerating income

From one year to another:

Not everything can be wrapped up by the end of the year. Accounting Today’s senior tax editor, Roger Russell, covers the issues from 2020 that will have an impact on 2021:

The tax impacts of remote work

How to handle emergency retirement plan withdrawals under the CARES Act

The taxability of unemployment benefits

In under the wire:

While many of them don’t need to be taken up by December 31st, the last-minute COVID relief legislation signed by President Trump included a number of tax provisions including:

The Tax Cuts and Jobs Acts (TCJA) limited the individual tax deduction of state and local taxes (SALT) to $10,000 for married filing joint and $5,000 for married fling separate, or single. We feel this limitation was done to offset tax reductions done to spur the US economy. This limitation hurt and increased income taxes for taxpayers that are residents in states with high taxes. Taxpayers and states have been looking for a method of getting around this tax deduction limitation. Various ideas have failed, but the IRS recently issued IRS Notice 2020-75 which provides some hope. In the notice the IRS is explaining that if a state makes a flow through entity (an S Corporation or Partnership) liable for the income tax, rather than the shareholders or partners, and the entity pays it, then that state tax is not limited. Many states have been looking for a way to help their residence, and the IRS has explained a way, but why hasn’t more states implemented this change if they really want to help their residence? Currently only seven (7) states have made this change.

Scope

The purpose of this memo is to discuss Notice 2020-75 issued by Internal Revenue Service (IRS) on November 9, 2020, which allows state and local income taxes imposed on and paid by partnerships or S Corporations in computing its non-separately stated taxable income or loss for the taxable year of payment and are not subject to SALT limitation.

Background

Tax Cuts and Job Acts (TCJA) limits the individual deduction of SALT to $10,000 (or $5,000 for married filing separately) for tax years 2018-2025. Due to this limitation, the notice cited that certain jurisdictions have enacted or contemplating to enact tax laws that impose either a mandatory or elective entity-level income tax on partnerships and S Corporations that do business in the jurisdiction or have income derived from or connected with sources within the jurisdiction. The notice pointed out that “certain jurisdictions provide a corresponding offsetting, owner-level tax benefit, such as full or partial credit, deduction, or exclusion” for taxes deducted at the Pass-Through Entity (PTE) level and that Treasury and IRS are “aware of the uncertainty as to whether entity level-payments made under these laws to jurisdictions described in §164(b)(2) other than U.S. territories must be taken into account in applying the SALT deduction limitation at the owner level”.

The notice also announced the IRS’s intention to issue a proposed regulation to provide clarity to individual owners of partnerships and S Corporations in calculating their SALT deduction limitations and clarify the Specified Income Tax Payments which are deductible by partnerships and S Corporations in computing their non-separately stated income or loss.

Discussion/Analysis

Reporting of Deduction in the Partnership or S Corporation Tax Return

Based on the notice, SALT does not need to be separately stated. Thus, it would be expected that the deduction will be reported under “Taxes and Licenses” on Form 1065 or 1120S and will flow-through to partners/shareholders as part of Box 1 “ordinary income or loss” on Schedule K-1.

Deductibility of the SALT

As mentioned in the notice, there are “certain jurisdictions” that shifted the individual tax to entity-level tax to “workaround” from the SALT limitation under TCJA and below are the states that imposes entity-level income tax which is referred to as a “Specified Income Tax Payment”:

Connecticut – effective January 1, 2018

Louisiana – election to be made

Maryland – imposed to the distributive shares or pro rata shares of resident members of the PTE

New Jersey – effective January 1, 2020, election to be made

Oklahoma – effective January 1, 2019, needs annual election

Rhode Island – effective January 1, 2019, election to be made

Wisconsin – effective January 1, 2019 for person or persons holding more than 50% of capital and profits of a partnership

According to the notice, if a partnership or an S Corporation makes a Specified Income Tax Payment during the taxable year, the partnership or S Corporation is allowed a deduction for the Specified Income Tax Payment in computing its taxable income for the taxable year in which the payment is made.

The impending proposed regulations defined “Specified Income Tax Payments” as any amount paid by a partnership or an S Corporation to a State, a political subdivision of a State or the District of Columbia (Domestic Jurisdiction) to satisfy its liability for income taxes imposed by the Domestic Jurisdiction on the partnership or S Corporation, meaning, it will solely include the state and local taxes paid under Sec. 164(b)(2) but excluding taxes paid or accrued to foreign countries and U.S. territories under Sec. 703(a)(2)(B) and Sec. 1363(b)(2).

Effectivity Date of the Deduction

Based on the notice, the forthcoming Proposed Regulations will apply to payments on or after November 9, 2020, but taxpayers are also permitted to apply the rules to payments made in a partnership or S Corporation tax year ending after December 31, 2017 and before November 9, 2020.

Notes/Comments

This is a taxpayer friendly decision made by IRS. It is expected that other states, particularly those that impose high personal income tax rates on residents that are disproportionately affected by the $10,000 SALT deduction cap may enact similar laws in response to IRS guidance.

Currently, California and many other high tax states have not made this beneficial change. If you live in a state with high income taxes, I suggest you contact them.

Individual states and every individual have unique tax calculations and applications of tax laws, so please contact us if you have questions.

Taxpayers should be alert to potential fake emails or websites looking to steal personal information. The IRS will never initiate contact with taxpayers via email about a tax bill, refund or Economic Impact Payments. Don’t click on links claiming to be from the IRS. Be wary of emails and websites − they may be nothing more than scams to steal personal information. VA Comment:We have been informed by a handful of our clients that they have received IRS emails. Please note that this is one of the top IRS scams. Make sure everyone in your accounting department knows this so you can reduce your risk of a financial crime.

IRS Criminal Investigation has seen a tremendous increase in phishing schemes utilizing emails, letters, texts and links. These phishing schemes are using keywords such as “coronavirus,” “COVID-19” and “Stimulus” in various ways.

These schemes are blasted to large numbers of people in an effort to get personal identifying information or financial account information, including account numbers and passwords. Most of these new schemes are actively playing on the fear and unknown of the virus and the stimulus payments. (For more see IR-2020-115, IRS warns against COVID-19 fraud; other financial schemes.)

Fake Charities:

Criminals frequently exploit natural disasters and other situations such as the current COVID-19 pandemic by setting up fake charities to steal from well-intentioned people trying to help in times of need. Fake charity scams generally rise during times like these.

Fraudulent schemes normally start with unsolicited contact by telephone, text, social media, e-mail or in-person using a variety of tactics. Bogus websites use names similar to legitimate charities to trick people to send money or provide personal financial information. They may even claim to be working for or on behalf of the IRS to help victims file casualty loss claims and get tax refunds.

Taxpayers should be particularly wary of charities with names like nationally known organizations. Legitimate charities will provide their Employer Identification Number (EIN), if requested, which can be used to verify their legitimacy. Taxpayers can find legitimate and qualified charities with the search tool on IRS.gov.

Threatening Impersonator Phone Calls:

IRS impersonation scams come in many forms. A common one remains bogus threatening phone calls from a criminal claiming to be with the IRS. The scammer attempts to instill fear and urgency in the potential victim. In fact, the IRS will never threaten a taxpayer or surprise him or her with a demand for immediate payment. VA Comments:If you receive a call from the IRS or any government authority, and you are not sure, please get their contact information and contact Vertical Advisors so we can assist quickly.

Phone scams or “vishing” (voice phishing) pose a major threat. Scam phone calls, including those threatening arrest, deportation or license revocation if the victim doesn’t pay a bogus tax bill, are reported year-round. These calls often take the form of a “robocall” (a text-to-speech recorded message with instructions for returning the call).

The IRS will never demand immediate payment, threaten, ask for financial information over the phone, or call about an unexpected refund or Economic Impact Payment. Taxpayers should contact the real IRS if they worry about having a tax problem.

Social Media Scams:

Taxpayers need to protect themselves against social media scams, which frequently use events like COVID-19 to try tricking people. Social media enables anyone to share information with anyone else on the Internet. Scammers use that information as ammunition for a wide variety of scams. These include emails where scammers impersonate someone’s family, friends or co-workers.

Social media scams have also led to tax-related identity theft. The basic element of social media scams is convincing a potential victim that he or she is dealing with a person close to them that they trust via email, text or social media messaging.

Using personal information, a scammer may email a potential victim and include a link to something of interest to the recipient which contains malware intended to commit more crimes. Scammers also infiltrate their victim’s emails and cell phones to go after their friends and family with fake emails that appear to be real and text messages soliciting, for example, small donations to fake charities that are appealing to the victims.

EIP or Refund Theft:

The IRS has made great strides against refund fraud and theft in recent years, but they remain an ongoing threat. Criminals this year also turned their attention to stealing Economic Impact Payments as provided by the Coronavirus Aid, Relief, and Economic Security (CARES) Act.

Much of this stems from identity theft whereby criminals file false tax returns or supply other bogus information to the IRS to divert refunds to wrong addresses or bank accounts.

The IRS recently warned nursing homes and other care facilities that Economic Impact Payments generally belong to the recipients, not the organizations providing the care. This came following concerns that people and businesses may be taking advantage of vulnerable populations who received the payments. These payments do not count as a resource for determining eligibility for Medicaid and other federal programs They also do not count as income in determining eligibility for these programs. See IR-2020-121, IRS alert: Economic Impact Payments belong to recipient, not nursing homes or care facilities for more.

Taxpayers can consult the Coronavirus Tax Relief page of IRS.gov for assistance in getting their EIPs. Anyone who believes they may be a victim of identity theft should consult the Taxpayer Guide to Identity Theft on IRS.gov.

Senior Fraud:

Senior citizens and those who care about them need to be on alert for tax scams targeting older Americans. The IRS recognizes the pervasiveness of fraud targeting older Americans along with the Department of Justice and FBI, the Federal Trade Commission, the Consumer Financial Protection Bureau (CFPB), among others.

Seniors are more likely to be targeted and victimized by scammers than other segments of society. Financial abuse of seniors is a problem among personal and professional relationships. Anecdotal evidence across professional services indicates that elder fraud goes down substantially when the service provider knows a trusted friend or family member is taking an interest in the senior’s affairs.

Older Americans are becoming more comfortable with evolving technologies, such as social media. Unfortunately, that gives scammers another means of taking advantage. Phishing scams linked to Covid-19 have been a major threat this filing season. Seniors need to be alert for a continuing surge of fake emails, text messages, websites and social media attempts to steal personal information.

Scams targeting non-English speakers:

IRS impersonators and other scammers also target groups with limited English proficiency. These scams are often threatening in nature. Some scams also target those potentially receiving an Economic Impact Payment and request personal or financial information from the taxpayer.

Phone scams pose a major threat to people with limited access to information, including individuals not entirely comfortable with the English language. These calls frequently take the form of a “robocall” (a text-to-speech recorded message with instructions for returning the call), but in some cases may be made by a real person. These con artists may have some of the taxpayer’s information, including their address, the last four digits of their Social Security number or other personal details – making the phone calls seem more legitimate.

A common one remains the IRS impersonation scam where a taxpayer receives a telephone call threatening jail time, deportation or revocation of a driver’s license from someone claiming to be with the IRS. Taxpayers who are recent immigrants often are the most vulnerable and should ignore these threats and not engage the scammers.

Unscrupulous Return Preparers:

Selecting the right return preparer is important. They are entrusted with a taxpayer’s sensitive personal data. Most tax professionals provide honest, high-quality service, but dishonest preparers pop up every filing season committing fraud, harming innocent taxpayers or talking taxpayers into doing illegal things they regret later.

Taxpayers should avoid so-called “ghost” preparers who expose their clients to potentially serious filing mistakes as well as possible tax fraud and risk of losing their refunds. With many tax professionals impacted by COVID-19 and their offices potentially closed, taxpayers should take particular care in selecting a credible tax preparer.

Ghost preparers don’t sign the tax returns they prepare. They may print the tax return and tell the taxpayer to sign and mail it to the IRS. For e-filed returns, the ghost preparer will prepare but not digitally sign as the paid preparer. By law, anyone who is paid to prepare or assists in preparing federal tax returns must have a Preparer Tax Identification Number (PTIN). Paid preparers must sign and include their PTIN on returns.

Unscrupulous preparers may also target those without a filing requirement and may or may not be due a refund. They promise inflated refunds by claiming fake tax credits, including education credits, the Earned Income Tax Credit (EITC) and others. Taxpayers should avoid preparers who ask them to sign a blank return, promise a big refund before looking at the taxpayer’s records or charge fees based on a percentage of the refund.

Taxpayers are ultimately responsible for the accuracy of their tax return, regardless of who prepares it. Taxpayers can go to a special page on IRS.gov for tips on choosing a preparer.

Offer in Compromise Mills:

Taxpayers need to wary of misleading tax debt resolution companies that can exaggerate chances to settle tax debts for “pennies on the dollar” through an Offer in Compromise (OIC). These offers are available for taxpayers who meet very specific criteria under law to qualify for reducing their tax bill. But unscrupulous companies oversell the program to unqualified candidates so they can collect a hefty fee from taxpayers already struggling with debt. VA Comment: We hear these ads often. We have had individuals contact us after companies that advertise to settle IRS debt for “pennies on the dollar” didn’t work. The IRS does have OIC program, but it can be very changelings to settle debt for “pennies on the dollar.”. We have never seen a settlement for “pennies on the dollar”.

These scams are commonly called OIC “mills,” which cast a wide net for taxpayers, charge them pricey fees and churn out applications for a program they’re unlikely to qualify for. Although the OIC program helps thousands of taxpayers each year reduce their tax debt, not everyone qualifies for an OIC. In Fiscal Year 2019, there were 54,000 OICs submitted to the IRS. The agency accepted 18,000 of them.

Individual taxpayers can use the free online Offer in Compromise Pre-Qualifier tool to see if they qualify. The simple tool allows taxpayers to confirm eligibility and provides an estimated offer amount. Taxpayers can apply for an OIC without third-party representation; but the IRS reminds taxpayers that if they need help, they should be cautious about whom they hire.

Fake Payments with Repayment Demands:

Criminals are always finding new ways to trick taxpayers into believing their scam including putting a bogus refund into the taxpayer’s actual bank account. Here’s how the scam works:

A con artist steals or obtains a taxpayer’s personal data including Social Security number or Individual Taxpayer Identification Number (ITIN) and bank account information. The scammer files a bogus tax return and has the refund deposited into the taxpayer’s checking or savings account. Once the direct deposit hits the taxpayer’s bank account, the fraudster places a call to them, posing as an IRS employee. The taxpayer is told that there’s been an error and that the IRS needs the money returned immediately or penalties and interest will result. The taxpayer is told to buy specific gift cards for the amount of the refund.

The IRS will never demand payment by a specific method. There are many payment options available to taxpayers and there’s also a process through which taxpayers have the right to question the amount of tax we say they owe. Anytime a taxpayer receives an unexpected refund and a call from us out of the blue demanding a refund repayment, they should reach out to their banking institution and to the IRS.

Payroll and HR Scams:

Tax professionals, employers and taxpayers need to be on guard against phishing designed to steal Form W-2s and other tax information. These are Business Email Compromise (BEC) or Business Email Spoofing (BES). This is particularly true with many businesses closed and their employees working from home due to COVID-19. Currently, two of the most common types of these scams are the gift card scam and the direct deposit scam.

In the gift card scam, a compromised email account is often used to send a request to purchase gift cards in various denominations. In the direct deposit scheme, the fraudster may have access to the victim’s email account (also known as an email account compromise or “EAC”). They may also impersonate the potential victim to have the organization change the employee’s direct deposit information to reroute their deposit to an account the fraudster controls.

BEC/BES scams have used a variety of ploys to include requests for wire transfers, payment of fake invoices as well as others. In recent years, the IRS has observed variations of these scams where fake IRS documents are used in to lend legitimacy to the bogus request. For example, a fraudster may attempt a fake invoice scheme and use what appears to be a legitimate IRS document to help convince the victim.

The Direct Deposit and other BEC/BES variations should be forwarded to the Federal Bureau of Investigation Internet Crime Complaint Center (IC3) where a complaint can be filed. The IRS requests that Form W-2 scams be reported to: phishing@irs.gov (Subject: W-2 Scam).

Ransomware:

This is a growing cybercrime. Ransomware is malware targeting human and technical weaknesses to infect a potential victim’s computer, network or server. Malware is a form of invasive software that is often frequently inadvertently downloaded by the user. Once downloaded, it tracks keystrokes and other computer activity. Once infected, ransomware looks for and locks critical or sensitive data with its own encryption. In some cases, entire computer networks can be adversely impacted.

Victims generally aren’t aware of the attack until they try to access their data, or they receive a ransom request in the form of a pop-up window. These criminals don’t want to be traced so they frequently use anonymous messaging platforms and demand payment in virtual currency such as Bitcoin.

Cybercriminals might use a phishing email to trick a potential victim into opening a link or attachment containing the ransomware. These may include email solicitations to support a fake COVID-19 charity. Cybercriminals also look for system vulnerabilities where human error is not needed to deliver their malware.

The IRS and its Security Summit partners have advised tax professionals and taxpayers to use the free, multi-factor authentication feature being offered on tax preparation software products. Use of the multi-factor authentication feature is a free and easy way to protect clients and practitioners’ offices from data thefts. Tax software providers also offer free multi-factor authentication protections on their Do-It-Yourself products for taxpayers.

Please call us at 949-756-8080 if we can be of assistance.

Here’s a list of five fun ways to teach kids about money, which will help them with financial literacy—and help parents so the kids aren’t living with us forever:

1. Toys

You can start very young teaching basics with toys such like these:

Piggy Bank

As early as age 2, there are toys like The Learning Journey Numbers and Colors Pig E Bank, which has colored coins the bank counts as you put them in the slot. You can get this toy for around $19.

Cash Register

Beginning with toddlers (around age 3), you can use a play cash register to let kids play “store” and understand the basics of money. This can help them learn how much money they have, how much they have left when they buy something, and how things add up when you buy multiple things. One popular cash register from Learning Resources costs about $30 on Amazon.

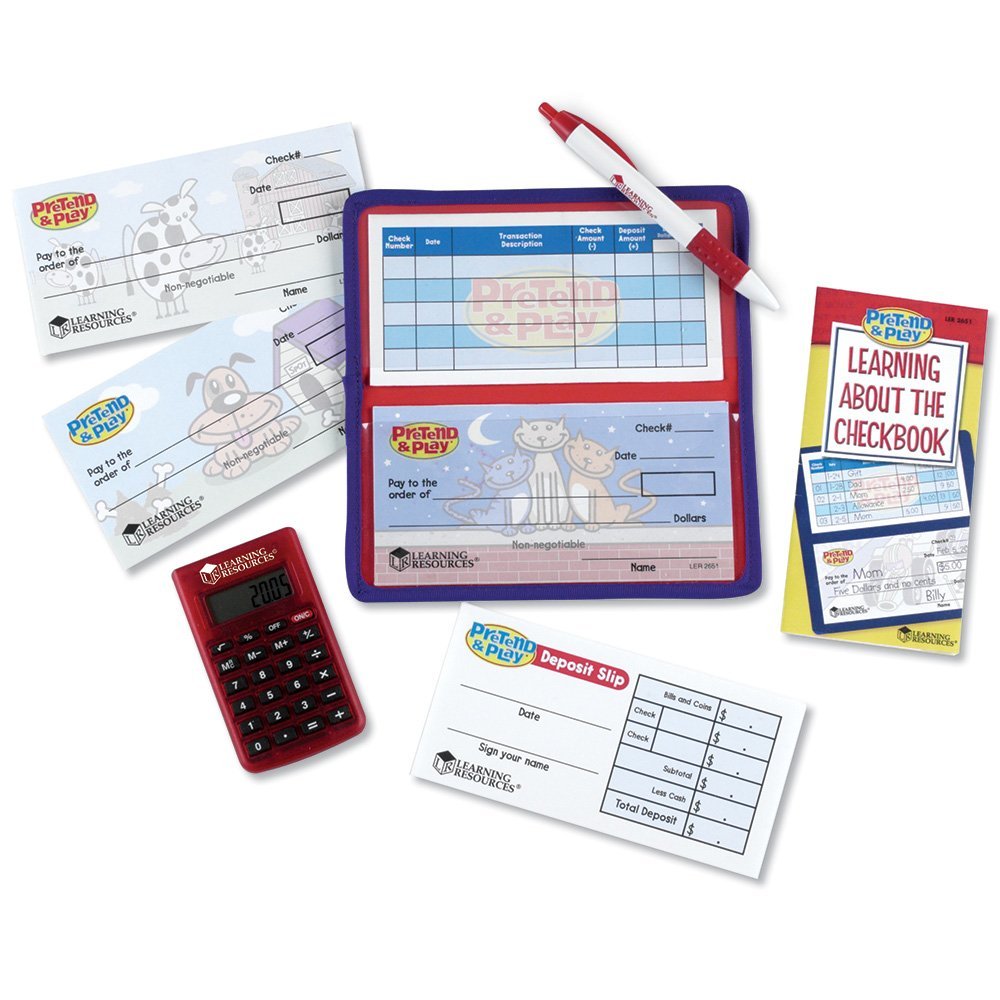

Checkbook

Made for kids 5 and up, this Learning Resources Pretend & Play Checkbook comes with a calculator, checkbook, deposit slips and guide to help kids learn about managing a bank account and writing checks. Even if checks aren’t often used much anymore, it’s still a fun way to help your kids learn about money and debiting accounts. It costs approximately $12.

2. Online Games

These games are available online for you to help your kids learn about money and finance:

Cash Puzzler

This simple money game on Visa’s Practical Money Skills site is made for ages 3-6 and involves putting together a “puzzle” from mixed up pieces of a bill ($1-$100).

Smart Money Commanders

Ruby’s Troupe is an organization that uses an interactive theatre with a fun-loving group of puppets to teach kids ages 3-10 (and their parents) about money and finance. The program was created by puppeteer Phyllis Mattson and Debbie Todd, a licensed CPA. It has online modules where children watch puppets, get coloring pages, and have access to games and activities.

“We have three purposes when it comes to teaching about managing money,” Todd explains. “First is for them to find out it’s fun. Second is to find out it’s practical. And third is that they can do it and be successful at it.”

They also focus lessons on the emotional and psychological aspects of money, because that is where a lot of mistakes can be made. They’ve also done live sessions and Todd says it’s amazing to see the “tall kids” (parents) sit in the back and learn with the kids: “By the end, we’ve provided the parents with the tools to have a non-confrontational, non-threatening conversation with their children.”

Ruby’s Troupe also donates 90% of its profits to charity, including nonprofits and foundations that promote financial literacy, which is critically lacking here in the U.S. Only 17 states offer financial literacy courses for high school students and a recent report card by Champlain College’s Center for Financial Literacy gave only five states—Alabama, Missouri, Tennessee, Utah, and Virginia—an ‘A’ grade for providing personal finance education.

Peter Pig’s Money Counter

Made for children from 5-8, this interactive game from Visa helps kids learn about counting and saving money along with U.S. currency.

Clay Piggy

Clay Piggy is an online game created for Kindergarten and above by a parent who didn’t find any fun options when trying to teach her own daughter about money. Students learn basic money management skills such as how to earn, spend, save, invest, and give.

There are different scenarios in the game where they have to take a job to earn money, create a budget, understand wants and needs, watch their credit scores, be a responsible investor by assessing credit profiles of other users who asking for loan, learn how to pay taxes, look at their paychecks and more.

“Parents need to talk to their children about savings and give them situations at an early age where they have to manage money,” explains Narinder Budhiraja, founder of Clay Piggy. “Lots of people learn about money by making mistakes and then spend lot of years fixing their mistakes. This bring lot of stress in their personal life. At Clay Piggy, we are determined to change that behavior.”

Currently Clay Piggy is currently only available for schools to use, but they’re planning to roll out an application for parents later this year.

Money Metropolis

Another game on Visa’s Practical Money Skills site, this one is created for 7-12 year olds to make life decisions that impact whether their virtual bank account will make or earn money.

Mt. Everest Money Simulation

This game is a choose-your-own-adventure simulation where kids help a backpacker plan a trip to Mt. Everest without going into debt. It’s available from Money Prodigy and is made for kids ages 8-13. You can learn more about it and join the wait list here.

Created for ages 13 and up, Cash Crunch 101 facilitates the conversation about money. It was created by a teacher for the classroom, but can be used by parents and kids as well.

3. Board Games

By keeping these around your house, your kids can play games with the family to learn more about money:

Monopoly Junior

Kids ages 5-8 can play a version of traditional Monopoly, learning how to count money and accumulate assets. It runs approximately $15.

Game of Life Junior

This version of Hasbro’s Game of Life is a version made for kids as young as 5 years old to go on various adventures and make money along the way. It costs about $25.

Cash Crunch Junior

This board game was created for children ages 7-12 and focuses on the value of money, denominations of money and making change. It’s a great way to help kids learn at home while having fun counting money. It costs $30 and is available on the Cash Crunch Games website.

Money Bags Coin Value Game

Kids ages 7 and older can play this board game from Learning Resources that teaches about collecting, counting and exchanging money. It costs about $16.

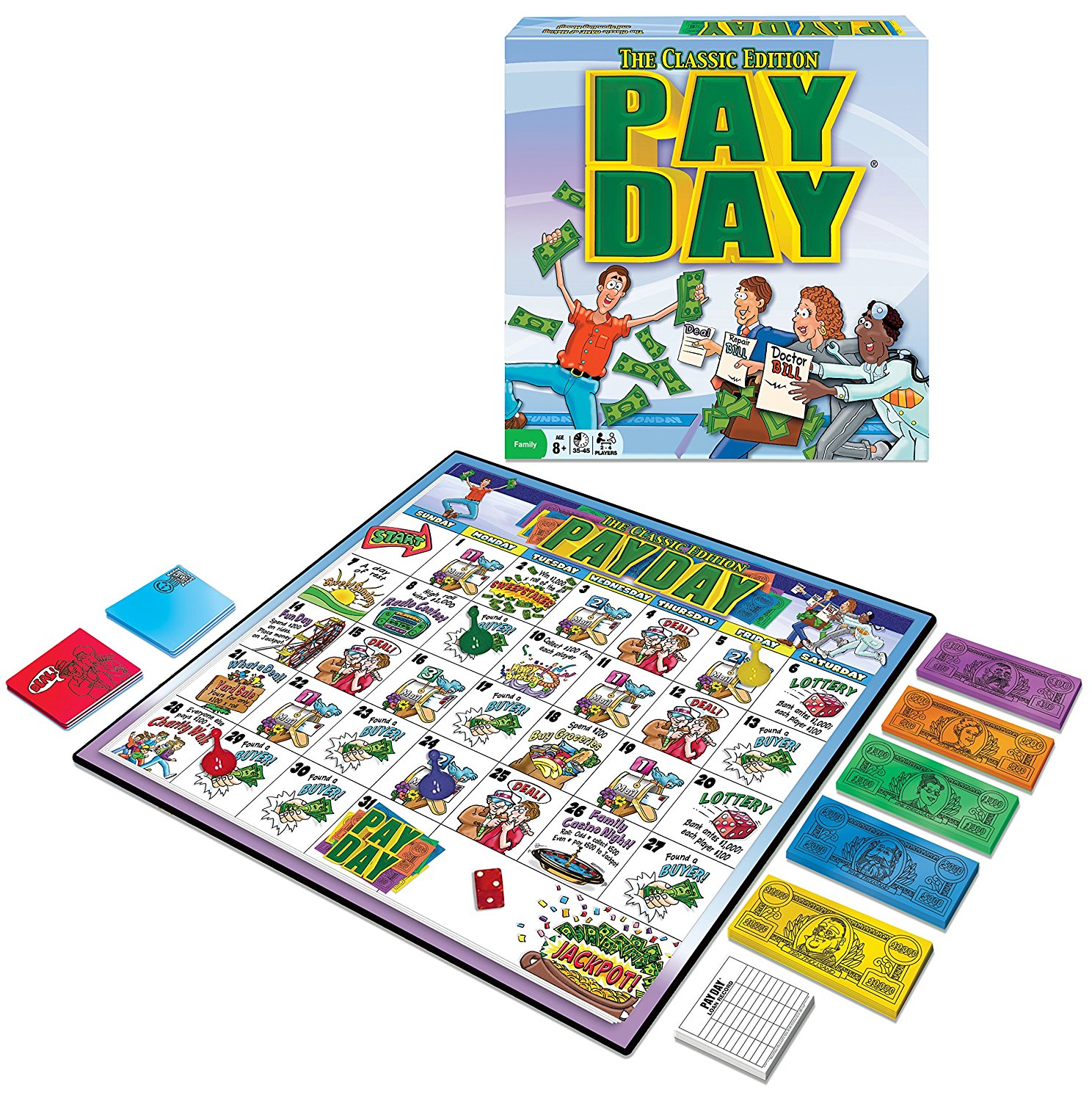

Pay Day

Originally launched in 1975, this board game was made for children 8 and older to play with their families. Created by Winning Moves Games, the object is to have the most money at the end of the game, which runs about 35-45 minutes long. Throughout the game, players can make deals on property to earn money, get a salary, pay off bills, take out loans, add to savings, and learn about paying fees. You can get it for approximately $15.

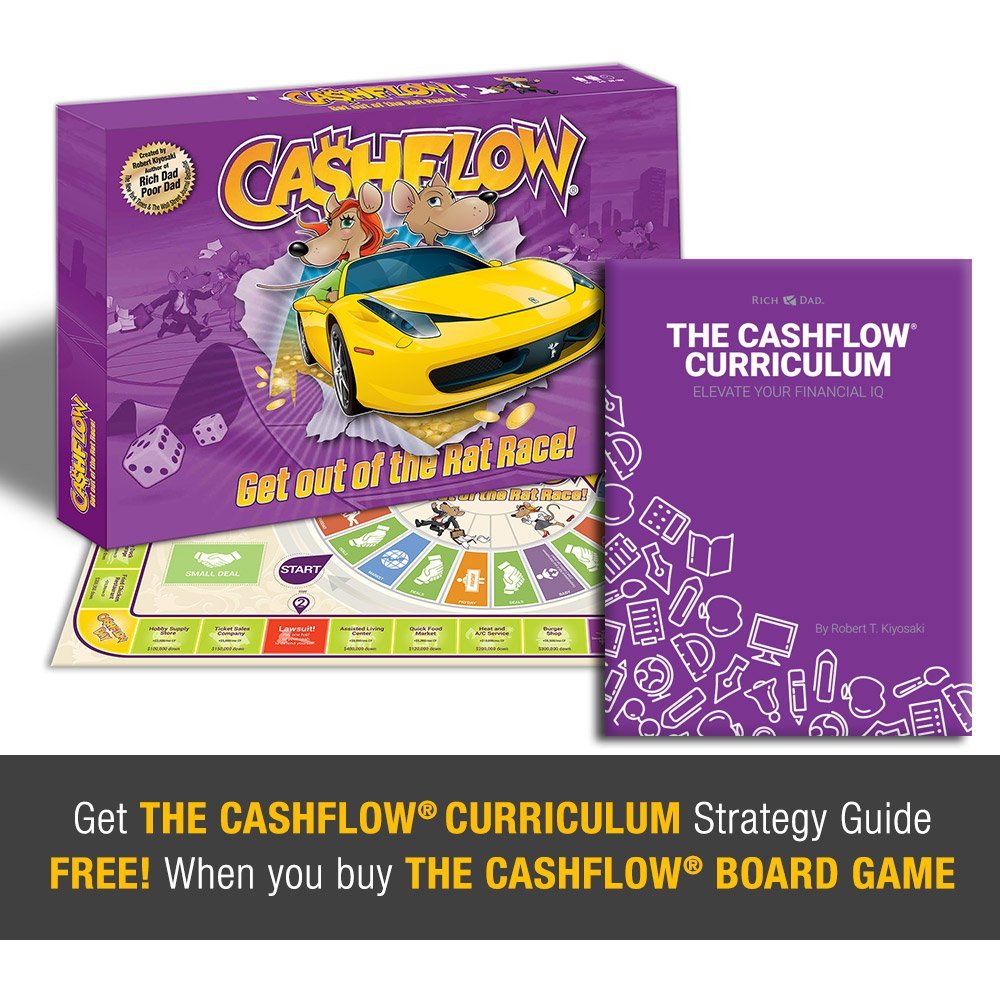

CASHFLOW

Ages 14 and up can learn more about financial skills, investing, and wealth building in a fun way with this interactive game. It was created by Robert Kiyosaki, author of the bestselling personal finance book of all time, Rich Dad Poor Dad, and comes with a PDF guide. The cost is approximately $80 on Amazon.

4. Activities & Outings

Money Museum

If you live in Chicago or are traveling there this summer, make sure to take your kids to the Chicago Fed’s Money Museum. It’s open Monday through Friday (except for Bank Holidays) and they offer exhibits such as the Alexander Hamilton Exhibit and interactive displays like the “Banker Challenge” game where kids play the role of a bank manager.

Summer Camps

While camps to get your kids outdoors are great, you may want to look into finance camps for a fun, educational experience for part of the summer. Even though finance summer camp may not sound exciting at first, these camps make money and entrepreneurship really fun for kids:

Camp BizSmartTM in Santa Clara, CA and Chattanooga, TN helps aspiring young entrepreneurs ages 11-15 learn how to solve business problems and defend their solution to executives and investors.

KidsCamps.com offers a directory of camps, showcasing availability in 18 states for business and finance camps.

Smart Money Commanders Fun Summer Money Games is launching its first online summer camp in mid-June 2018, which will run through August 2018.

Check out the children museum(s) in your area. Many of them have rotating exhibits and some of those cover business, money and finance in fun, interactive ways. You can find children’s museums here.

5. Charitable Activities

Teaching your kids how to give to others while on a budget is something that will help them learn various skills and allow them to feel a sense of purpose and pride. Here are some unique ways kids can learn about money and give back:

Kids Boost

There’s an organization in Atlanta, GA that not only encourages children to give back, but teaches them how to raise money. Kids Boost, which currently has a wait list of over 200 kids, is a 501(c)3 organization that gives children from third grade through high school $100 and they put together a fundraiser for a charity of their choice. In just a few years, they’ve given kids $6,000 and they have turned that into more than $110,000, supporting 48 non-profits.

“Fundraising comes with important life lessons such as money management, communication, planning, and accountability,” explains Kids Boost founder and executive director Kristen Wintzel. “This teaches kids so many things while boosting courage and self-esteem and supporting wonderful nonprofits around the world. Most kids go on to either compete another Kids Boost project or continue to get involved in philanthropy and civil engagement. Giving is powerful and giving is contagious!”

Birthday Gift Donations

Instead of adding to the never-ending supply of toys that your kids play with for five minutes, you can use your child’s birthday as an opportunity to give back. Some charities like St. Jude’s offer a birthday fundraising program where you can easily create a page to collect donations for your birthday. Also, Facebook lets you create a fundraiser for various organizations, letting you share and have people donate to anytime including your birthday.

You can also pick a charity that may need physical items and create an Amazon wish list. We did this with my daughter for her birthday—collected toys for the Aflac Cancer and Blood Disorders Center, an idea I borrowed from my cousin. You can deliver the items with your child and make them part of the experience.

This may not seem like its teaching kids how to manage money, but it helps them learn about wants vs. needs and the value of money—along with how it can be used to do good things for others.

Open Communication About Money

The bottom line is that you should get your kids involved in money conversations early on, and make sure it doesn’t become a taboo topic. That will benefit them (and you) in the long run because often times people get embarrassed when dealing with money challenges.

The unfortunate reality, though, is that many people deal with financial issues. A recent survey by the American Psychiatric Association shows that two-thirds of Americans are anxious about paying their bills, up from 56% last year. So the earlier you teach your kids about money and how to talk about it, the better they’ll be set up for success as they grow and have to make their own financial decisions.

For those who may not know where to start, Amanda Grossman, Certified Financial Education Instructor and founder of Money Prodigy says, “The best way parents can get started teaching their kids about money is to find out what your child is interested in, such as goals and what they want to be, do, and have in their lives. You can then tie any money lessons you teach or money conversations you have moving forward to their list of things that are important to them, meaning they’ll be more receptive in receiving the information instead of just thinking you’re babbling on about stuff that doesn’t relate to them.”